You see it all the time

"Building wealth has little to do with your income or investment returns, and lots to do with your savings rate." - Morgan Housel

8/13/20252 min read

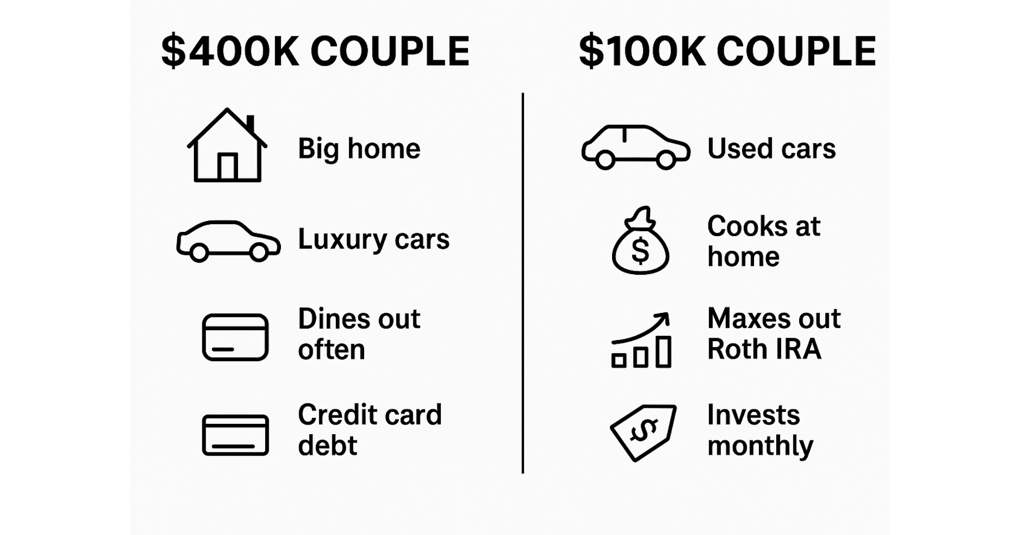

One couple earns $400,000 a year, they live in a big, beautiful home, drives luxury cars, dine out regularly, and carry five figures in credit card debt.

Another couple earns $100,000. They drive the same used cars they’ve had since college, cook most meals at home, max out their Roth IRAs, and invest every month through dollar cost averaging.

Fast-forward 10, 20, 30 years...guess who ends up wealthy?

Hint: It’s not the ones keeping up with the Joneses.

Why? Because wealth isn’t what you earn, it’s what you keep.

The $100K couple gets it. They:

Live below their means (smaller home, older cars, etc.)

Save 20%+ of their annual income

Mitigate lifestyle creep as salaries grow

Avoid high interest debt

Let compound interest do the heavy lifting

Meanwhile, the $400K couple is stuck in the income trap. As income rises, so do their expenses. Property taxes, high insurance costs, excessive luxury spending all add up. They look successful on the outside, but they are one recession away from significant financial stress.

The 50/30/20 Income Rule: A Quick Guide

50% - Needs (housing, utilities, insurance, food)

30% - Wants (travel, subscriptions, dining out)

20% - Savings & investing (emergency fund, retirement, brokerage account)

The younger you are and the fewer responsibilities you have the more you should save. 20% is a great starting point, it's not a ceiling. If you can save or invest more, do it. Hold yourself accountable or find someone to do it for you. You'll thank yourself later.

Real wealth is quiet

It’s the growing brokerage account. The paid-off house. The freedom to work less and eventually, not at all. It’s peace of mind.

This newsletter is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. All investments involve risk, including the possible loss of principal. Past performance is not indicative of future results. Iron Valley Investments is a registered investment adviser in the State of Pennsylvania. Registration does not imply a certain level of skill or training. A copy of Iron Valley Investments current written disclosure statement discussing Iron Valley Investments business operations, services, and fees is available at the SEC’s investment adviser public information website – www.adviserinfo.sec.gov or from Iron Valley Investments upon written request.